Hyperparameter Tuning (Supplementary Notebook)¶

This notebook explores a grid search with repeated k-fold cross validation scheme for tuning the hyperparameters of the LightGBM model used in forecasting the M5 dataset. In general, the techniques used below can be also be adapted for other forecasting models, whether they be classical statistical models or machine learning methods.

Prepared by: Sebastian C. Ibañez

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import lightgbm as lgb

from sklearn.model_selection import cross_val_score

from sklearn.model_selection import RepeatedKFold

plt.rcParams['figure.figsize'] = [15, 5]

np.set_printoptions(precision = 6, suppress = True)

### CREATE X,Y ####

def create_xy(series, window_size, prediction_horizon, shuffle = False):

x = []

y = []

for i in range(0, len(series)):

if len(series[(i + window_size):(i + window_size + prediction_horizon)]) < prediction_horizon:

break

x.append(series[i:(i + window_size)])

y.append(series[(i + window_size):(i + window_size + prediction_horizon)])

x = np.array(x)

y = np.array(y)

return x,y

date_list = [d.strftime('%Y-%m-%d') for d in pd.date_range(start = '2011-01-29', end = '2016-04-24')]

df_sales = pd.read_csv('../data/m5/sales_train_validation.csv')

df_sales.rename(columns = dict(zip(df_sales.columns[6:], date_list)), inplace = True)

df_sales_total_by_store = df_sales.groupby(['store_id']).sum()

series = df_sales_total_by_store.iloc[0]

### HYPERPARAMETERS ###

window_size = 365

prediction_horizon = 1

### TRAIN VAL SPLIT ### (include shuffling later)

test_size = 28

split_time = len(series) - test_size

train_series = series[:split_time]

test_series = series[split_time - window_size:]

train_x, train_y = create_xy(train_series, window_size, prediction_horizon)

test_x, test_y = create_xy(test_series, window_size, prediction_horizon)

train_y = train_y.flatten()

test_y = test_y.flatten()

model = lgb.LGBMRegressor(first_metric_only = True)

model.fit(train_x, train_y,

eval_metric = 'l1',

eval_set = [(test_x, test_y)],

early_stopping_rounds = 10,

verbose = 0)

forecast = model.predict(test_x)

s1_naive = series[-29:-1].to_numpy()

s7_naive = series[-35:-7].to_numpy()

s30_naive = series[-56:-28].to_numpy()

s365_naive = series[-364:-336].to_numpy()

print(' Naive MAE: %.4f' % (np.mean(np.abs(s1_naive - test_y))))

print(' s7-Naive MAE: %.4f' % (np.mean(np.abs(s7_naive - test_y))))

print(' s30-Naive MAE: %.4f' % (np.mean(np.abs(s30_naive - test_y))))

print('s365-Naive MAE: %.4f' % (np.mean(np.abs(s365_naive - test_y))))

print(' LightGBM MAE: %.4f' % (np.mean(np.abs(forecast - test_y))))

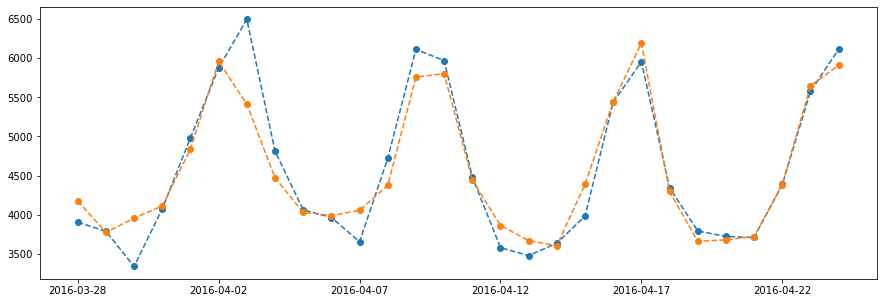

series[-test_size:].plot(marker = 'o', linestyle = '--')

plt.plot(forecast, marker = 'o', linestyle = '--')

plt.show()

Naive MAE: 698.0000

s7-Naive MAE: 372.2857

s30-Naive MAE: 330.8214

s365-Naive MAE: 247.9286

LightGBM MAE: 208.9156

Hyperparameter Tuning¶

Number of Trees¶

trees = [10, 50, 100, 500, 1000, 2000]

results = []

names = []

for i in trees:

params = {

'n_estimators': i,

}

cv = RepeatedKFold(n_splits = 10, n_repeats = 3, random_state = 1)

scores = cross_val_score(lgb.LGBMRegressor(**params), train_x, train_y, scoring = 'neg_mean_absolute_error', cv = cv, n_jobs = -1)

results.append(scores)

names.append(i)

print('%3d --- MAE: %.3f (%.3f)' % (i, np.mean(scores), np.std(scores)))

plt.boxplot(results, labels = names, showmeans = True)

plt.show()

10 --- MAE: -385.639 (31.537)

50 --- MAE: -283.540 (21.324)

Tree Depth¶

results = []

names = []

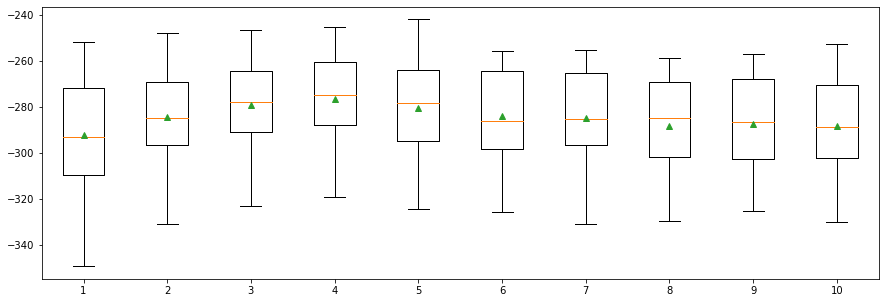

for i in range(1, 11):

params = {

'max_depth': i,

'num_leaves': 2**i,

}

cv = RepeatedKFold(n_splits = 10, n_repeats = 3, random_state = 1)

scores = cross_val_score(lgb.LGBMRegressor(**params), train_x, train_y, scoring = 'neg_mean_absolute_error', cv = cv, n_jobs = -1)

results.append(scores)

names.append(i)

print('%3d --- MAE: %.3f (%.3f)' % (i, np.mean(scores), np.std(scores)))

plt.boxplot(results, labels = names, showmeans = True)

plt.show()

1 --- MAE: -292.235 (24.008)

2 --- MAE: -284.534 (20.113)

3 --- MAE: -278.984 (20.519)

4 --- MAE: -276.622 (21.169)

5 --- MAE: -280.497 (21.999)

6 --- MAE: -283.877 (21.382)

7 --- MAE: -284.667 (21.436)

8 --- MAE: -288.216 (21.230)

9 --- MAE: -287.373 (21.043)

10 --- MAE: -288.503 (20.929)

Learning Rate¶

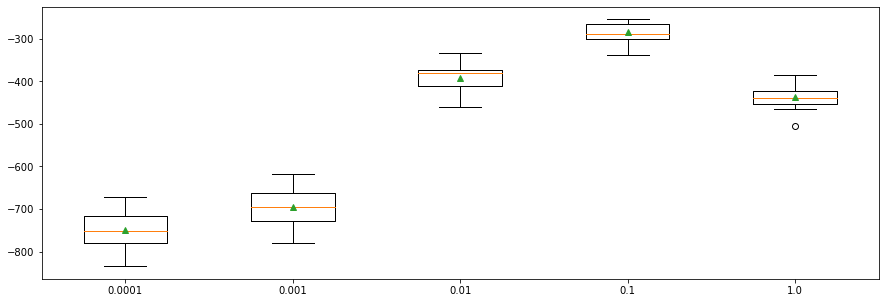

rates = [0.0001, 0.001, 0.01, 0.1, 1.0]

results = []

names = []

for i in rates:

params = {

'learning_rate': i,

}

cv = RepeatedKFold(n_splits = 10, n_repeats = 3, random_state = 1)

scores = cross_val_score(lgb.LGBMRegressor(**params), train_x, train_y, scoring = 'neg_mean_absolute_error', cv = cv, n_jobs = -1)

results.append(scores)

names.append(i)

print('%.3f --- MAE: %.3f (%.3f)' % (i, np.mean(scores), np.std(scores)))

plt.boxplot(results, labels = names, showmeans = True)

plt.show()

0.000 --- MAE: -748.947 (39.458)

0.001 --- MAE: -695.973 (38.578)

0.010 --- MAE: -391.718 (30.680)

0.100 --- MAE: -285.091 (21.551)

1.000 --- MAE: -437.648 (23.715)

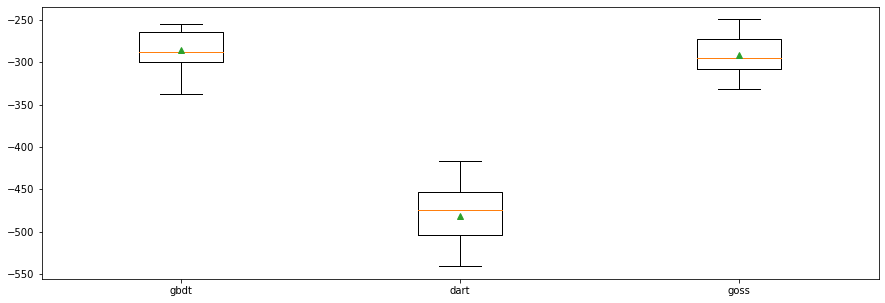

Boosting Type¶

gbdt: Gradient Boosting Decision Tree (GDBT).dart: Dropouts meet Multiple Additive Regression Trees (DART).goss: Gradient-based One-Side Sampling (GOSS).

types = ['gbdt', 'dart', 'goss']

results = []

names = []

for i in types:

params = {

'boosting_type': i,

}

cv = RepeatedKFold(n_splits = 10, n_repeats = 3, random_state = 1)

scores = cross_val_score(lgb.LGBMRegressor(**params), train_x, train_y, scoring = 'neg_mean_absolute_error', cv = cv, n_jobs = -1)

results.append(scores)

names.append(i)

print('%s --- MAE: %.3f (%.3f)' % (i, np.mean(scores), np.std(scores)))

plt.boxplot(results, labels = names, showmeans = True)

plt.show()

gbdt --- MAE: -285.091 (21.551)

dart --- MAE: -481.225 (33.006)

goss --- MAE: -291.263 (21.742)

More than one variable…¶

types = ['gbdt', 'dart', 'goss']

results = []

for i in types:

for j in range(1, 11):

params = {

'n_estimators': 2000,

'learning_rate': 0.1,

'max_depth': j,

'num_leaves': 2**j,

'boosting_type': i,

}

cv = RepeatedKFold(n_splits = 10, n_repeats = 3, random_state = 1)

scores = cross_val_score(lgb.LGBMRegressor(**params), train_x, train_y, scoring = 'neg_mean_absolute_error', cv = cv, n_jobs = -1)

results.append(scores)

print('%s %d --- MAE: %.3f (%.3f)' % (i, j, np.mean(scores), np.std(scores)))

gbdt 1 --- MAE: -287.860 (21.319)

gbdt 2 --- MAE: -298.625 (20.007)

gbdt 3 --- MAE: -288.742 (21.788)

gbdt 4 --- MAE: -284.235 (20.843)

gbdt 5 --- MAE: -285.302 (21.250)

gbdt 6 --- MAE: -288.334 (21.073)

gbdt 7 --- MAE: -288.306 (21.382)

gbdt 8 --- MAE: -290.893 (21.207)

/opt/conda/lib/python3.8/site-packages/joblib/externals/loky/process_executor.py:688: UserWarning: A worker stopped while some jobs were given to the executor. This can be caused by a too short worker timeout or by a memory leak.

warnings.warn(

gbdt 9 --- MAE: -291.163 (22.049)

gbdt 10 --- MAE: -291.799 (21.347)

dart 1 --- MAE: -277.039 (21.229)

dart 2 --- MAE: -278.634 (19.236)

dart 3 --- MAE: -274.650 (21.226)

dart 4 --- MAE: -274.975 (22.260)

dart 5 --- MAE: -276.816 (22.355)

dart 6 --- MAE: -278.424 (22.700)

dart 7 --- MAE: -280.250 (22.238)

dart 8 --- MAE: -281.548 (23.202)

dart 9 --- MAE: -282.776 (23.881)

dart 10 --- MAE: -283.613 (23.785)

goss 1 --- MAE: -301.392 (22.057)

goss 2 --- MAE: -305.135 (17.874)

goss 3 --- MAE: -297.664 (18.621)

goss 4 --- MAE: -297.698 (19.858)

goss 5 --- MAE: -296.022 (18.470)

goss 6 --- MAE: -295.540 (20.386)

goss 7 --- MAE: -290.380 (19.665)

goss 8 --- MAE: -295.496 (20.014)

goss 9 --- MAE: -292.827 (20.048)

goss 10 --- MAE: -293.961 (22.087)

Final Model¶

params = {

'n_estimators': 2000,

'max_depth': 4,

'num_leaves': 2**4,

'learning_rate': 0.1,

'boosting_type': 'dart'

}

model = lgb.LGBMRegressor(first_metric_only = True, **params)

model.fit(train_x, train_y,

eval_metric = 'l1',

eval_set = [(test_x, test_y)],

#early_stopping_rounds = 10,

verbose = 0)

forecast = model.predict(test_x)

s1_naive = series[-29:-1].to_numpy()

s7_naive = series[-35:-7].to_numpy()

s30_naive = series[-56:-28].to_numpy()

s365_naive = series[-364:-336].to_numpy()

print(' Naive MAE: %.4f' % (np.mean(np.abs(s1_naive - test_y))))

print(' s7-Naive MAE: %.4f' % (np.mean(np.abs(s7_naive - test_y))))

print(' s30-Naive MAE: %.4f' % (np.mean(np.abs(s30_naive - test_y))))

print('s365-Naive MAE: %.4f' % (np.mean(np.abs(s365_naive - test_y))))

print(' LightGBM MAE: %.4f' % (np.mean(np.abs(forecast - test_y))))

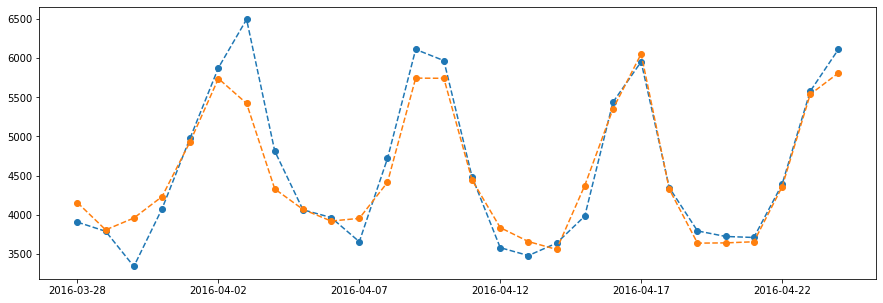

series[-test_size:].plot(marker = 'o', linestyle = '--')

plt.plot(forecast, marker = 'o', linestyle = '--')

plt.show()

Naive MAE: 698.0000

s7-Naive MAE: 372.2857

s30-Naive MAE: 330.8214

s365-Naive MAE: 247.9286

LightGBM MAE: 200.5037