Chapter 3: Vector Autoregressive Methods¶

Prepared by: Maria Eloisa Ventura

Previously, we have introduced the classical approaches in forecasting single/univariate time series like the ARIMA (autoregressive integrated moving-average) model and the simple linear regression model. We learned that stationarity is a condition that is necessary when using ARIMA while this need not be imposed when using the linear regression model. In this notebook, we extend the forecasting problem to a more generalized framework where we deal with multivariate time series–time series which has more than one time-dependent variable. More specifically, we introduce vector autoregressive (VAR) models and show how they can be used in forecasting mutivariate time series.

Multivariate Time Series Model¶

As shown in the previous chapters, one of the main advantages of using simple univariate methods (e.g., ARIMA) is the ability to forecast future values of one variable by only using past values of itself. However, we know that most if not all of the variables that we observe are actually dependent on other variables. Most of the time, the information that we gather is limited by our capacity to measure the variables of interest. For example, if we want to study weather in a particular city, we could measure temperature, humidity and precipitation over time. But if we only have a thermometer, then we’ll only be able to collect data for temperature, effectively reducing our dataset to a univariate time series.

Now, in cases where we have multiple time series (longitudinal measurements of more than one variable), we can actually use multivariate time series models to understand the relationships of the different variables over time. By utilizing the additional information available from related series, these models can often provide better forecasts than the univariate time series models.

In this section, we cover the foundational information needed to understand Vector Autoregressive Models, a class of multivariate time series models, by using a framework similar to univariate time series laid out in the previous chapters, and extending it to the multivariate case.

Definition: Univariate vs Multivariate Time Series¶

Time series can either be univariate or multivariate. The term univariate time series consists of single observations recorded sequentially over equal time increments. When dealing with a univariate time series model (e.g., ARIMA), we usually refer to a model that contains lag values of itself as the independent variable.

On the other hand, a multivariate time series has more than one time-dependent variable. For a multivariate process, several related time series are observed simultaneously over time. As an extension of the univariate case, the multivariate time series model involves two or more input variables, and leverages the interrelationship among the different time series variables.

import numpy as np

import pandas as pd

import statsmodels.tsa as tsa

from statsmodels.tsa.vector_ar.var_model import VAR, FEVD

from statsmodels.tsa.arima_model import ARIMA

from statsmodels.tsa.stattools import acf, adfuller, ccf, ccovf, kpss

from statsmodels.graphics.tsaplots import plot_acf

import matplotlib.pyplot as plt

import mvts_utils as utils

import seaborn as sns

import warnings

warnings.filterwarnings("ignore")

pd.set_option('display.max_rows', None)

pd.set_option('display.max_columns', None)

%load_ext autoreload

%autoreload 2

Example 1: Multivariate Time Series¶

A. Air Quality Data from UCI¶

The dataset contains hourly averaged measurements obtained from an Air Quality Chemical Multisensor Device which was located on the field of a polluted area at an Italian city. The dataset can be downloaded here.

aq_df = pd.read_excel("../data/AirQualityUCI/AirQualityUCI.xlsx", parse_dates=[['Date', 'Time']])\

.set_index('Date_Time').replace(-200, np.nan).interpolate()

aq_df.head(2)

| CO(GT) | PT08.S1(CO) | NMHC(GT) | C6H6(GT) | PT08.S2(NMHC) | NOx(GT) | PT08.S3(NOx) | NO2(GT) | PT08.S4(NO2) | PT08.S5(O3) | T | RH | AH | Unnamed: 15 | Unnamed: 16 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date_Time | |||||||||||||||

| 2004-03-10 00:00:00 18:00:00 | 2.6 | 1360.00 | 150.0 | 11.881723 | 1045.50 | 166.0 | 1056.25 | 113.0 | 1692.00 | 1267.50 | 13.6 | 48.875001 | 0.757754 | NaN | NaN |

| 2004-03-10 00:00:00 19:00:00 | 2.0 | 1292.25 | 112.0 | 9.397165 | 954.75 | 103.0 | 1173.75 | 92.0 | 1558.75 | 972.25 | 13.3 | 47.700000 | 0.725487 | NaN | NaN |

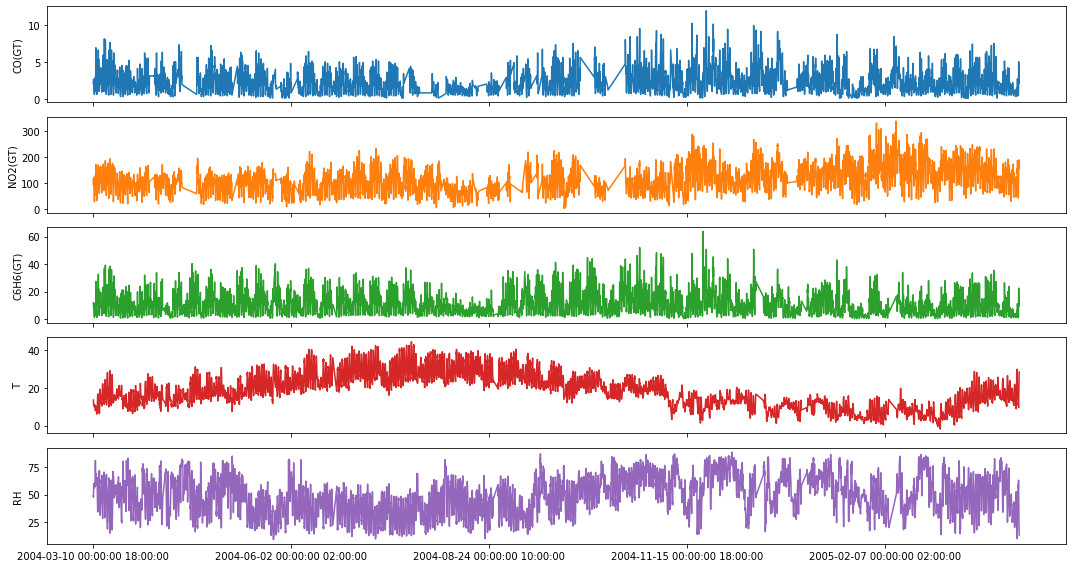

fig,ax = plt.subplots(5, figsize=(15,8), sharex=True)

plot_cols = ['CO(GT)', 'NO2(GT)', 'C6H6(GT)', 'T', 'RH']

aq_df[plot_cols].plot(subplots=True, legend=False, ax=ax)

for a in range(len(ax)):

ax[a].set_ylabel(plot_cols[a])

ax[-1].set_xlabel('')

plt.tight_layout()

plt.show()

B. Global Health from The World Bank¶

This dataset combines key health statistics from a variety of sources to provide a look at global health and population trends. It includes information on nutrition, reproductive health, education, immunization, and diseases from over 200 countries. The dataset can be downloaded here.

ind_df = pd.read_csv('../data/WorldBankHealth/WorldBankHealthPopulation_SeriesSummary.csv')\

.loc[:,['series_code', 'indicator_name']].drop_duplicates().reindex()\

.sort_values('indicator_name').set_index('series_code')

hn_df = pd.read_csv('../data/WorldBankHealth/WorldBankHealthPopulation_HealthNutritionPopulation.csv')\

.pivot(index='year', columns='indicator_code', values='value')

cols = ['SH.XPD.KHEX.GD.ZS', 'SH.XPD.CHEX.GD.ZS', 'SH.XPD.GHED.GD.ZS']

health_expenditure_df = hn_df.loc[np.arange(2000, 2018), cols]\

.rename(columns = dict(ind_df.loc[cols].indicator_name\

.apply(lambda x: '_'.join(x.split('(')[0].split(' ')[:-1]))))

health_expenditure_df.index = pd.date_range('2000-1-1', periods=len(health_expenditure_df), freq="A-DEC")

health_expenditure_df.head(3)

| indicator_code | Capital_health_expenditure | Current_health_expenditure | Domestic_general_government_health_expenditure |

|---|---|---|---|

| 2000-12-31 | 0.013654 | 3.154818 | 1.400685 |

| 2001-12-31 | 0.012675 | 2.947059 | 1.196554 |

| 2002-12-31 | 0.018476 | 2.733301 | 1.012481 |

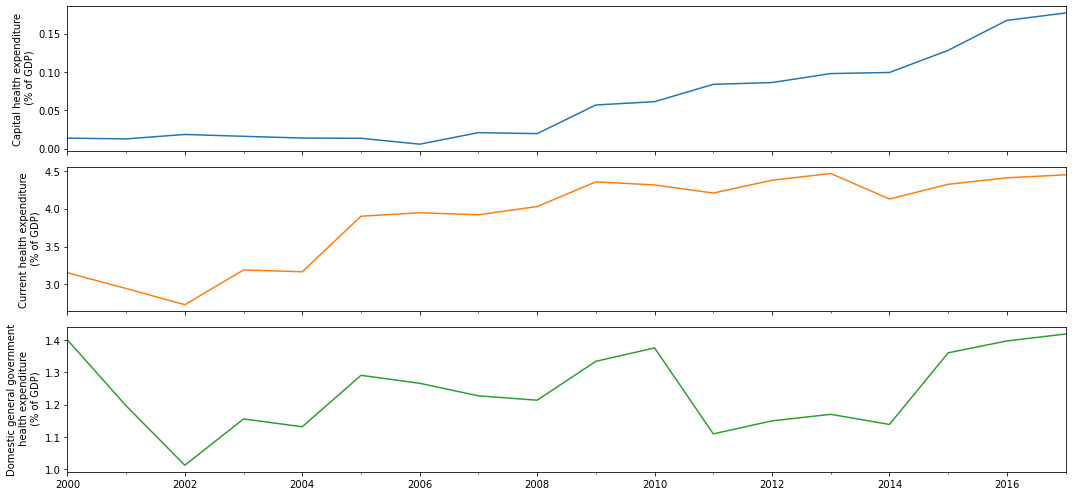

fig, ax = plt.subplots(3, 1, sharex=True, figsize=(15,7))

health_expenditure_df.plot(subplots=True, ax=ax, legend=False)

y_label = ['Capital health expenditure', 'Current health expenditure',

'Domestic general government\n health expenditure']

for a in range(len(ax)):

ax[a].set_ylabel(f"{y_label[a]}\n (% of GDP)")

plt.tight_layout()

plt.show()

C. US Treasury Rates¶

January, 1982 – December, 2016 (Weekly) https://essentialoftimeseries.com/data/ This sample dataset contains weekly data of US Treasury rates from January 1982 to December 2016. The dataset can be downloaded here.

treas_df = pd.read_excel("../data/USTreasuryRates/us-treasury-rates-weekly.xlsx")

treas_df = treas_df.rename(columns={'Unnamed: 0': 'Date'}).set_index('Date')

treas_df.index = pd.to_datetime(treas_df.index)

treas_df.head(3)

| 1-month | 3-month | 6-month | 1-year | 2-year | 3-year | 5-year | 7-year | 10-year | Excess CRSP Mkt Returns | 10-year Treasury Returns | Term spread | Change in term spread | 5-year Treasury Returns | Unnamed: 15 | Excess 10-year Treasury Returns | Term Spread | VXO | Delta VXO | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||

| 1982-01-08 | 10.296 | 12.08 | 13.36 | 13.80 | 14.12 | 14.32 | 14.46 | 14.54 | 14.47 | -1.632 | NaN | 2.39 | NaN | NaN | NaN | -0.286662 | 1.729559 | 20.461911 | -0.003106 |

| 1982-01-15 | 10.296 | 12.72 | 13.89 | 14.39 | 14.67 | 14.73 | 14.79 | 14.84 | 14.76 | -2.212 | -2.9 | 2.04 | -0.35 | 1.65 | -2.556 | -3.758000 | 4.464000 | NaN | NaN |

| 1982-01-22 | 10.296 | 13.47 | 14.30 | 14.72 | 14.93 | 14.92 | 14.81 | 14.80 | 14.73 | -0.202 | 0.3 | 1.26 | -0.78 | 0.10 | 0.049 | -0.558000 | 4.434000 | NaN | NaN |

fig,ax = plt.subplots(1, figsize=(15, 3), sharex=True)

data_df = treas_df.iloc[:, 0:9]

data_df.plot(ax=ax)

plt.ylabel('US Treasury yield (%)')

plt.xlabel('')

plt.legend(ncol=2)

plt.tight_layout()

plt.show()

D. Jena Climate Data¶

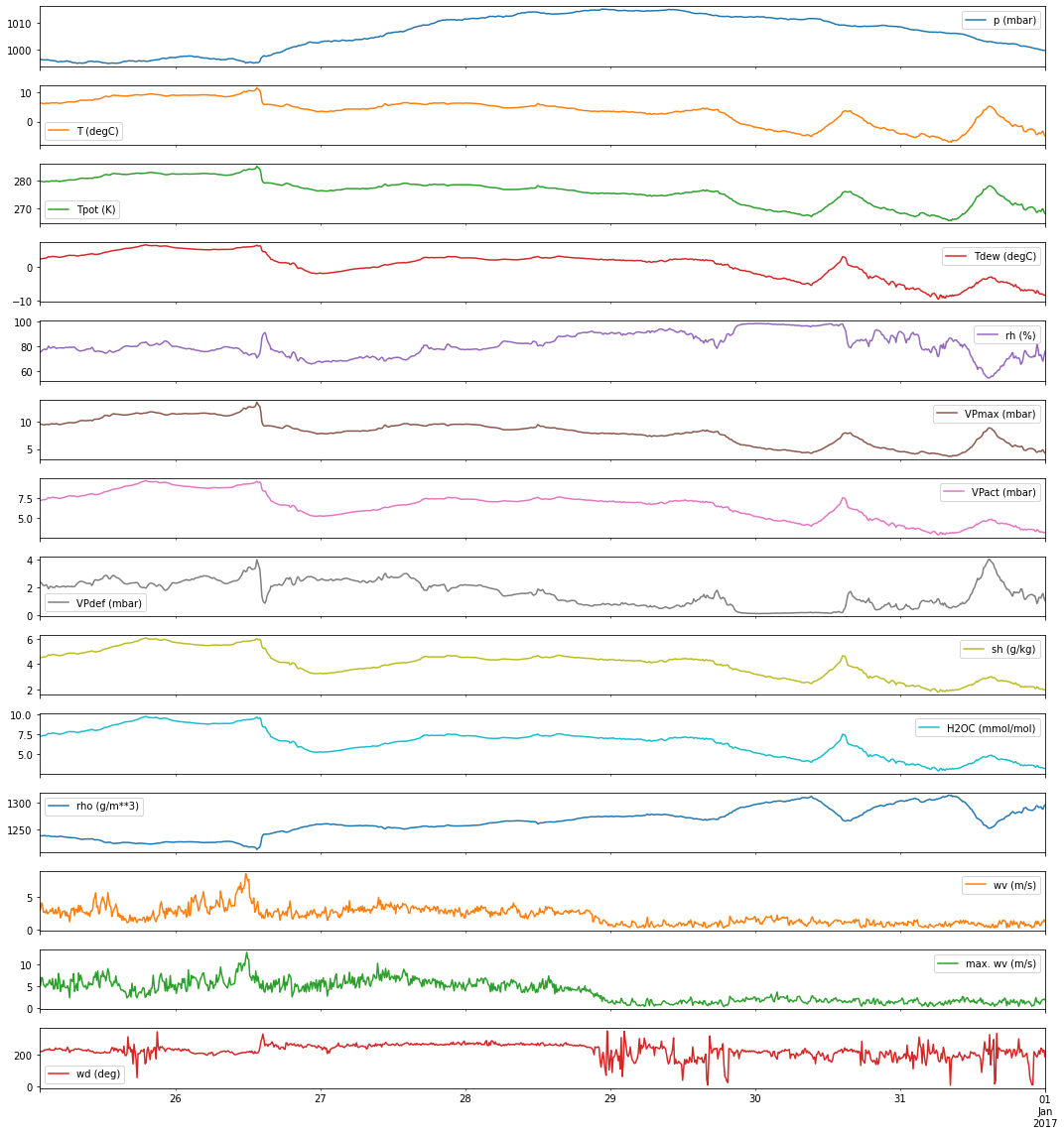

Time series dataset recorded at the Weather Station at the Max Planck Institute for Biogeochemistry in Jena, Germany from 2009 to 2016. It contains 14 different quantities (e.g., air temperature, atmospheric pressure, humidity, wind direction, and so on) were recorded every 10 minutes. You can download the data here.

jena_data = pd.read_csv('../data/jena_climate_2009_2016.csv')

jena_data['Date Time'] = pd.to_datetime(jena_data['Date Time'])

jena_data = jena_data.set_index('Date Time')

jena_data.head(3)

fig,ax = plt.subplots(jena_data.shape[-1], figsize=(15,16), sharex=True)

jena_data.iloc[-1000:].plot(subplots=True, ax=ax)

ax[-1].set_xlabel('')

plt.tight_layout()

plt.show()

Foundations¶

Before we discuss VARs, we outline some fundamental concepts below that we will need to understand the model.

Weak Stationarity of Multivariate Time Series¶

As in the univariate case, one of the requirements that we need to satisfy before we can apply VAR models is stationarity–in particular, weak stationarity. Both in the univariate and multivariate case, the first two moments of the time series are time-invariant. More formally, we describe weak stationarity below.

Consider a \(N\)-dimensional time series, \(\mathbf{y}_t = \left[y_{1,t}, y_{2,t}, ..., y_{N,t}\right]^\prime\). This is said to be weakly stationary if the first two moments are finite and constant through time, that is,

\(E\left[\mathbf{y}_t\right] = \boldsymbol{\mu}\)

\(E\left[(\mathbf{y}_t-\boldsymbol{\mu})(\mathbf{y}_t-\boldsymbol{\mu})^\prime\right] \equiv \boldsymbol\Gamma_0 < \infty\) for all \(t\)

\(E\left[(\mathbf{y}_t-\boldsymbol{\mu})(\mathbf{y}_{t-h}-\boldsymbol{\mu})^\prime\right] \equiv \boldsymbol\Gamma_h\) for all \(t\) and \(h\)

where the expectations are taken element-by-element over the joint distribution of \(\mathbf{y}_t\):

\(\boldsymbol{\mu}\) is the vector of means \(\boldsymbol\mu = \left[\mu_1, \mu_2, ..., \mu_N \right]\)

\(\boldsymbol\Gamma_0\) is the \(N\times N\) covariance matrix where the \(i\)th diagonal element is the variance of \(y_{i,t}\), and the \((i, j)\)th element is the covariance between \(y_{i,t}\) and \({y_{j,t}}\)

\(\boldsymbol\Gamma_h\) is the cross-covariance matrix at lag \(h\)

Obtaining Cross-Correlation Matrix from Cross-Covariance Matrix¶

When dealing with a multivariate time series, we can examine the predictability of one variable on another by looking at the relationship between them using the cross-covariance function (CCVF) and cross-correlation function (CCF). To do this, we begin by defining the cross-covariance between two variables, then we estimate the cross-correlation between one variable and another variable that is time-shifted. This informs us whether one time series may be related to the past lags of the other. In other words, CCF is used for identifying lags of one variable that might be useful as a predictor of the other variable.

At lag 0:

Let \(\mathbf\Gamma_0\) be the covariance matrix at lag 0, \(\mathbf D\) be a \(N\times N\) diagonal matrix containing the standard deviations of \(y_{i,t}\) for \(i=1, ..., N\). The correlation matrix of \(\mathbf{y}_t\) is defined as

where the \((i, j)\)th element of \(\boldsymbol\rho_0\) is the correlation coefficient between \(y_{i,t}\) and \(y_{j,t}\) at time \(t\):

At lag h:

Let \(\boldsymbol\Gamma_h = E\left[(\mathbf{y}_t-\boldsymbol{\mu})(\mathbf{y}_{t-h}-\boldsymbol{\mu})^\prime\right]\) be the lag-\(h\) covariance cross-covariance matrix of \(\mathbf y_{t}\). The lag-\(h\) cross-correlation matrix is defined as

The \((i,j)\)th element of \(\boldsymbol\rho_h\) is the correlation coefficient between \(y_{i,t}\) and \(y_{j,t-h}\):

What do we get from this?

Correlation Coefficient |

Interpretation |

|---|---|

\(\rho_{i,j}(0)\neq0\) |

\(y_{i,t}\) and \(y_{j,t}\) are contemporaneously linearly correlated |

\(\rho_{i,j}(h)=\rho_{j,i}(h)=0\) for all \(h\geq0\) |

\(y_{i,t}\) and \(y_{j,t}\) share no linear relationship |

\(\rho_{i,j}(h)=0\) and \(\rho_{j,i}(h)=0\) for all \(h>0\) |

\(y_{i,t}\) and \(y_{j,t}\) are said to be linearly uncoupled |

\(\rho_{i,j}(h)=0\) for all \(h>0\), but \(\rho_{j,i}(q)\neq0\) for at least some \(q>0\) |

There is a unidirectional (linear) relationship between \(y_{i,t}\) and \(y_{j,t}\), where \(y_{i,t}\) does not depend on \(y_{j,t}\), but \(y_{j,t}\) depends on (some) lagged values of \(y_{i,t}\) |

\(\rho_{i,j}(h)\neq0\) for at least some \(h>0\) and \(\rho_{j,i}(q)\neq0\) for at least some \(q>0\) |

There is a bi-directional (feedback) linear relationship between \(y_{i,t}\) and \(y_{j,t}\) |

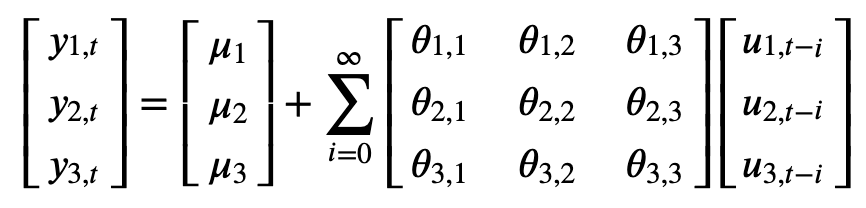

Vector Autoregressive (VAR) Models¶

The vector autoregressive (VAR) model is one of the most successful models for analysis of multivariate time series. It has been demonstrated to be successful in describing relationships and forecasting economic and financial time series, and providing more accurate forecasts than the univariate time series models and theory-based simultaneous equations models.

The structure of the VAR model is just the generalization of the univariate AR model. It is a system regression model that treats all the variables as endogenous, and allows each of the variables to depend on \(p\) lagged values of itself and of all the other variables in the system.

A VAR model of order \(p\) can be represented as

where \(\mathbf y_t\) is a \(N\times 1\) vector containing \(N\) endogenous variables, \(\mathbf a_0\) is a \(N\times 1\) vector of constants, \(\mathbf A_1, \mathbf A_2, ..., \mathbf A_p\) are the \(p\) \(N\times N\) matrices of autoregressive coefficients, and \(\mathbf u_t\) is a \(N\times 1\) vector of white noise disturbances.

VAR(1) Model¶

To illustrate, let’s consider the simplest VAR model where we have \(p=1\).

Structural and Reduced Forms of the VAR model¶

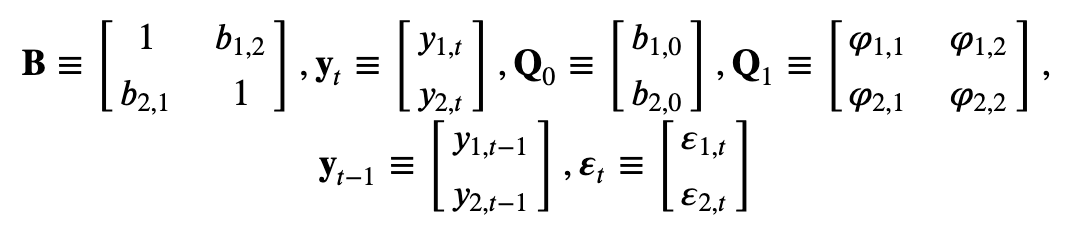

Consider the following bivariate system

where both \(y_{1,t}\) and \(y_{2,t}\) are assumed to be stationary, and \(\varepsilon_{1,t}\) and \(\varepsilon_{2,t}\) are the uncorrelated error terms with standard deviation \(\sigma_{1,t}\) and \(\sigma_{2,t}\), respectively.

In matrix notation:

Let

then

Structural VAR (VAR in primitive form)¶

Described by equation above

Captures contemporaneous feedback effects (\(b_{1,2}, b_{2,1}\))

Not very practical to use

Contemporaneous terms cannot be used in forecasting

Needs further manipulation to make it more useful (e.g. multiplying the matrix equation by \(\mathbf B^{-1}\))

Multiplying the matrix equation by \(\mathbf B^{-1}\), we get

or

where \(\mathbf a_0 = \mathbf B^{-1}\mathbf Q_0\), \(\mathbf A_1 = \mathbf B^{-1}\mathbf Q_1\), \(L\) is the lag/backshift operator, and \(\mathbf u_t = \mathbf B^{-1}\boldsymbol\varepsilon_t\), equivalently,

Reduced-form VAR (VAR in standard form)¶

Described by equation above

Only dependent on lagged endogenous variables (no contemporaneous feedback)

Can be estimated using ordinary least squares (OLS)

VMA infinite representation and Stationarity¶

Consider the reduced form, standard VAR(1) model

Assuming that the process is weakly stationary and taking the expectation of \(\mathbf y_t\), we have

where \(E\left[\mathbf u_t\right]=0.\) If we let \(\tilde{\mathbf y}_{t}\equiv \mathbf y_t - \boldsymbol \mu\) be the mean-corrected time-series, we can write the model as

Substituting \(\tilde{\mathbf y}_{t-1} = \mathbf A_1 \tilde{\mathbf y}_{t-2} + \mathbf u_{t-1}\),

If we keep iterating, we get

Letting \(\boldsymbol\Theta_i\equiv A_1^i\), we get the VMA infinite representation

Stationarity of the VAR(1) model¶

All the N eigenvalues of the matrix \(A_1\) must be less than 1 in modulus, to avoid that the coefficient matrix \(A_1^j\) from either exploding or converging to a nonzero matrix as \(j\) goes to infinity.

Provided that the covariance matrix of \(u_t\) exists, the requirement that all the eigenvalues of \(A_1\) are less than one in modulus is a necessary and sufficient condition for \(y_t\) to be stable, and thus, stationary.

All roots of \(det\left(\mathbf I_N - \mathbf A_1 z\right)=0\) must lie outside the unit circle.

VAR(p) Model¶

Consider the VAR(p) model described by

Using the lag operator \(L\), we get

where \(\tilde{\mathbf A} (L) = (\mathbf I_N - A_1 L - ... - A_p L^p)\). Assuming that \(\mathbf y_t\) is weakly stationary, we obtain that

Defining \(\tilde{\mathbf y}_t=\mathbf y_t -\boldsymbol\mu\), we have

Properties¶

\(Cov[\mathbf y_t, \mathbf u_t] = \Sigma_u\), the covariance matrix of \(\mathbf u_t\)

\(Cov[\mathbf y_{t-h}, \mathbf u_t] = \mathbf 0\) for any \(h>0\)

\(\boldsymbol\Gamma_h = \mathbf A_1 \boldsymbol\Gamma_{h-1} +...+\mathbf A_p \boldsymbol\Gamma_{h-p}\) for \(h>0\)

\(\boldsymbol\rho_h = \boldsymbol \Psi_1 \boldsymbol\Gamma_{h-1} +...+\boldsymbol \Psi_p \boldsymbol\Gamma_{h-p}\) for \(h>0\), where \(\boldsymbol \Psi_i = \mathbf D^{-1/2}\mathbf A_i D^{-1/2}\)

Stationarity of VAR(p) model¶

All roots of \(det\left(\mathbf I_N - \mathbf A_1 z - ...- \mathbf A_p z^p\right)=0\) must lie outside the unit circle.

Specification of a VAR model: Choosing the order p¶

Fitting a VAR model involves the selection of a single parameter: the model order or lag length \(p\). The most common approach in selecting the best model is choosing the \(p\) that minimizes one or more information criteria evaluated over a range of model orders. The criterion consists of two terms: the first one characterizes the entropy rate or prediction error, and second one characterizes the number of freely estimated parameters in the model. Minimizing both terms will allow us to identify a model that accurately models the data while preventing overfitting (due to too many parameters).

Some of the commonly used information criteria include: Akaike Information Criterion (AIC), Schwarz’s Bayesian Information Criterion (BIC), Hannan-Quinn Criterion (HQ), and Akaike’s Final Prediction Error Criterion (FPE). The equation for each are shown below.

Akaike’s information criterion

Schwarz’s Bayesian information criterion

Hannan-Quinn’s information criterion

Final prediction error

where \(M\) stands for multivariate, \(\tilde{\boldsymbol\Sigma}_u\) is the estimated covariance matrix of the residuals, \(T\) is the number of observations in the sample, and \(k\) is the total number of equations in the VAR(\(p\)) (i.e. \(N^2p + N\) where \(N\) is the number of equations and \(p\) is the number of lags).

Among the metrics above, AIC and BIC are the most widely used criteria, but BIC penalizes higher orders more. For moderate and large sample sizes, AIC and FPE are essentially equivalent, but FPE may outperform AIC for small sample sizes. HQ also penalizes higher order models more heavily than AIC, but less than BIC. However, under small sample conditions, AIC/FPE may outperform BIC and/or HQ in selecting true model order.

There are cases when AIC and FPE show no clear minimum over a range or model orders or lag lengths. In this case, there may be a clear “elbow” when we plot the values over model order. This may indicate a suitable model order.

Building a VAR model¶

In this section, we show how we can use the VAR model to forecast the air quality data. The following steps are shown below:

Check for stationarity.

Split data into train and test sets.

Select the VAR order p that gives.

Fit VAR model of order p on the train set.

Generate forecast.

Evaluate model performance.

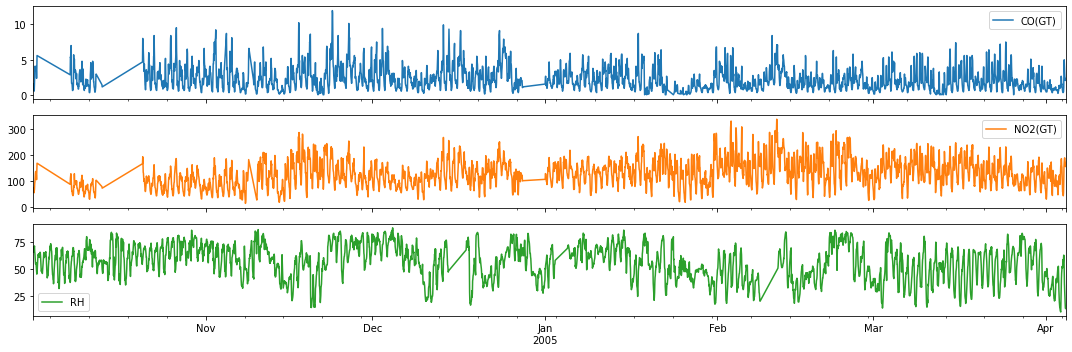

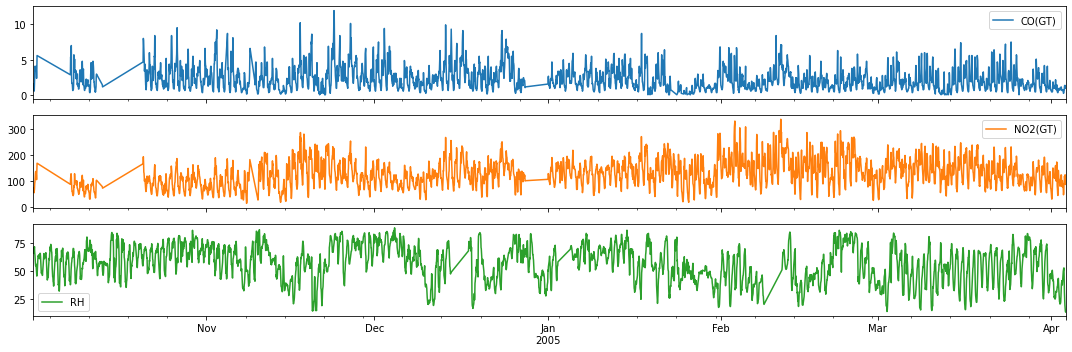

Example 2: Forecasting Air Quality Data (CO, NO2 and RH)¶

For illustration, we consider the carbon monoxide, nitrous dioxide and relative humidity time series from the Air Quality Dataset from 1 October 2014.

cols = ['CO(GT)', 'NO2(GT)', 'RH']

data_df = aq_df.loc[aq_df.index>'2004-10-01',cols]

fig,ax = plt.subplots(3, figsize=(15,5), sharex=True)

data_df.plot(ax=ax, subplots=True)

plt.xlabel('')

plt.tight_layout()

plt.show()

Quick inspection before we proceed with modeling…

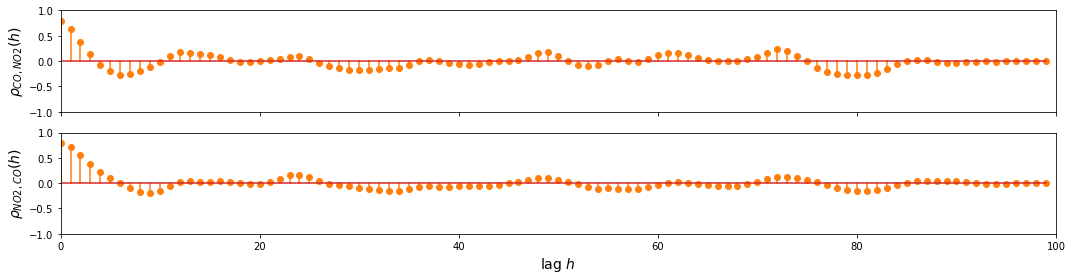

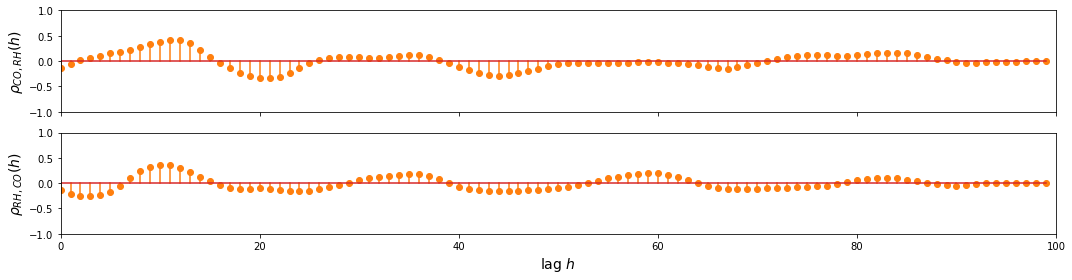

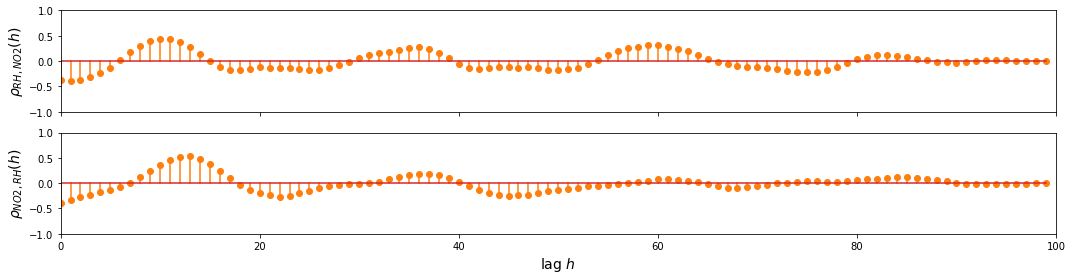

To find out whether the multivariate approach is better than treating the signals separately as univariate time series, we examine the relationship between the variables using CCF. The sample below shows the CCF for the last 100 data points of the Air quality data for CO, NO2 and RH.

CO and NO2

sample_df = data_df.iloc[-100:]

ccf_y1_y2 = ccf(sample_df['CO(GT)'], sample_df['NO2(GT)'], unbiased=False)

ccf_y2_y1 = ccf(sample_df['NO2(GT)'], sample_df['CO(GT)'], unbiased=False)

fig, ax = plt.subplots(2, figsize=(15, 4), sharex=True, sharey=True)

d=1

ax[0].stem(np.arange(len(sample_df))[::d], ccf_y1_y2[::d], linefmt='C1-', markerfmt='C1o')

ax[1].stem(np.arange(len(sample_df))[::d], ccf_y2_y1[::d], linefmt='C1-', markerfmt='C1o')

ax[-1].set_ylim(-1, 1)

ax[0].set_xlim(0, 100)

ax[-1].set_xlabel('lag $h$', fontsize=14)

ax[0].set_ylabel(r'$\rho_{CO,NO2} (h)$', fontsize=14)

ax[1].set_ylabel(r'$\rho_{NO2,CO} (h)$', fontsize=14)

plt.tight_layout()

plt.show()

CO and RH

ccf_y1_y2 = ccf(sample_df['CO(GT)'], sample_df['RH'], unbiased=False)

ccf_y2_y1 = ccf(sample_df['RH'], sample_df['CO(GT)'], unbiased=False)

fig, ax = plt.subplots(2, figsize=(15, 4), sharex=True, sharey=True)

d=1

ax[0].stem(np.arange(len(sample_df))[::d], ccf_y1_y2[::d], linefmt='C1-', markerfmt='C1o')

ax[1].stem(np.arange(len(sample_df))[::d], ccf_y2_y1[::d], linefmt='C1-', markerfmt='C1o')

ax[-1].set_ylim(-1, 1)

ax[0].set_xlim(0, 100)

ax[-1].set_xlabel('lag $h$', fontsize=14)

ax[0].set_ylabel(r'$\rho_{CO,RH} (h)$', fontsize=14)

ax[1].set_ylabel(r'$\rho_{RH,CO} (h)$', fontsize=14)

plt.tight_layout()

plt.show()

RH and NO2

ccf_y1_y2 = ccf(sample_df['RH'], sample_df['NO2(GT)'], unbiased=False)

ccf_y2_y1 = ccf(sample_df['NO2(GT)'], sample_df['RH'], unbiased=False)

fig, ax = plt.subplots(2, figsize=(15, 4), sharex=True, sharey=True)

d=1

ax[0].stem(np.arange(len(sample_df))[::d], ccf_y1_y2[::d], linefmt='C1-', markerfmt='C1o')

ax[1].stem(np.arange(len(sample_df))[::d], ccf_y2_y1[::d], linefmt='C1-', markerfmt='C1o')

ax[-1].set_ylim(-1, 1)

ax[0].set_xlim(0, 100)

ax[-1].set_xlabel('lag $h$', fontsize=14)

ax[0].set_ylabel(r'$\rho_{RH,NO2} (h)$', fontsize=14)

ax[1].set_ylabel(r'$\rho_{NO2,RH} (h)$', fontsize=14)

plt.tight_layout()

plt.show()

Observation/s:

As shown in the plot above, we can see that there’s a relationship between:

CO and some lagged values of RH and NO2

NO2 and some lagged values of RH and CO

RH and some lagged values of CO and NO2

This shows that we can benefit from the multivariate approach, so we proceed with building the VAR model.

1. Check stationarity¶

To check for stationarity, we use the Kwiatkowski–Phillips–Schmidt–Shin (KPSS) test and the Augmented Dickey-Fuller (ADF) test. For the data to be suitable for VAR modelling, we need each of the variables in the multivariate time series to be stationary. In both tests, we need the test statistic to be less than the critical values to say that a time series (a variable) to be stationary.

Kwiatkowski–Phillips–Schmidt–Shin (KPSS) test¶

Recall: Null hypothesis is that an observable time series is stationary around a deterministic trend (i.e. trend-stationary) against the alternative of a unit root.

test_stat, p_val = [], []

cv_1pct, cv_2p5pct, cv_5pct, cv_10pct = [], [], [], []

for c in data_df.columns:

kpss_res = kpss(data_df[c].dropna(), regression='ct')

test_stat.append(kpss_res[0])

p_val.append(kpss_res[1])

cv_1pct.append(kpss_res[3]['1%'])

cv_2p5pct.append(kpss_res[3]['1%'])

cv_5pct.append(kpss_res[3]['5%'])

cv_10pct.append(kpss_res[3]['10%'])

kpss_res_df = pd.DataFrame({'Test statistic': test_stat,

'p-value': p_val,

'Critical value - 1%': cv_1pct,

'Critical value - 2.5%': cv_2p5pct,

'Critical value - 5%': cv_5pct,

'Critical value - 10%': cv_10pct},

index=data_df.columns).T

kpss_res_df.round(4)

| CO(GT) | NO2(GT) | RH | |

|---|---|---|---|

| Test statistic | 0.0702 | 0.3239 | 0.1149 |

| p-value | 0.1000 | 0.0100 | 0.1000 |

| Critical value - 1% | 0.2160 | 0.2160 | 0.2160 |

| Critical value - 2.5% | 0.2160 | 0.2160 | 0.2160 |

| Critical value - 5% | 0.1460 | 0.1460 | 0.1460 |

| Critical value - 10% | 0.1190 | 0.1190 | 0.1190 |

Observation/s:

From the KPSS test, CO and RH are stationary.

Augmented Dickey-Fuller (ADF) test¶

Recall: Null hypothesis is that a unit root is present in a time series sample against the alternative that the time series is stationary.

test_stat, p_val = [], []

cv_1pct, cv_5pct, cv_10pct = [], [], []

for c in data_df.columns:

adf_res = adfuller(data_df[c].dropna())

test_stat.append(adf_res[0])

p_val.append(adf_res[1])

cv_1pct.append(adf_res[4]['1%'])

cv_5pct.append(adf_res[4]['5%'])

cv_10pct.append(adf_res[4]['10%'])

adf_res_df = pd.DataFrame({'Test statistic': test_stat,

'p-value': p_val,

'Critical value - 1%': cv_1pct,

'Critical value - 5%': cv_5pct,

'Critical value - 10%': cv_10pct},

index=data_df.columns).T

adf_res_df.round(4)

| CO(GT) | NO2(GT) | RH | |

|---|---|---|---|

| Test statistic | -7.0195 | -6.7695 | -6.8484 |

| p-value | 0.0000 | 0.0000 | 0.0000 |

| Critical value - 1% | -3.4318 | -3.4318 | -3.4318 |

| Critical value - 5% | -2.8622 | -2.8622 | -2.8622 |

| Critical value - 10% | -2.5671 | -2.5671 | -2.5671 |

Observation/s:

From the ADF test, CO, NO2 and RH are stationary.

2. Split data into train and test sets¶

We use the dataset from 01 October 2014 to predict the last 24 points (24 hrs/1 day) in the dataset.

forecast_length = 24

train_df, test_df = data_df.iloc[:-forecast_length], data_df.iloc[-forecast_length:]

test_df = test_df.filter(test_df.columns[~test_df.columns.str.contains('-d')])

train_df.reset_index().to_csv('../data/AirQualityUCI/train_data.csv')

test_df.reset_index().to_csv('../data/AirQualityUCI/test_data.csv')

fig,ax = plt.subplots(3, figsize=(15, 5), sharex=True)

train_df.plot(ax=ax, subplots=True)

plt.xlabel('')

plt.tight_layout()

plt.show()

3. Select order p¶

We compute the different multivariate information criteria (AIC, BIC, HQIC), and FPE. We pick the set of order parameters that correspond to the lowest values.

aic, bic, fpe, hqic = [], [], [], []

model = VAR(train_df)

p = np.arange(1,60)

for i in p:

result = model.fit(i)

aic.append(result.aic)

bic.append(result.bic)

fpe.append(result.fpe)

hqic.append(result.hqic)

lags_metrics_df = pd.DataFrame({'AIC': aic,

'BIC': bic,

'HQIC': hqic,

'FPE': fpe},

index=p)

fig, ax = plt.subplots(1, 4, figsize=(15, 3), sharex=True)

lags_metrics_df.plot(subplots=True, ax=ax, marker='o')

plt.tight_layout()

Observation/s:

We find BIC and HQIC to be lowest at \(p=26\), and we also observe an elbow in the plots for AIC, and FPE, so we choose the number of lags to be 26.

3. Fit VAR model with chosen order¶

%%time

var_model = model.fit(26)

var_model.summary()

CPU times: user 401 ms, sys: 39.9 ms, total: 441 ms

Wall time: 202 ms

Summary of Regression Results

==================================

Model: VAR

Method: OLS

Date: Sun, 21, Feb, 2021

Time: 00:47:42

--------------------------------------------------------------------

No. of Equations: 3.00000 BIC: 7.42717

Nobs: 4404.00 HQIC: 7.20458

Log likelihood: -34107.4 FPE: 1191.88

AIC: 7.08328 Det(Omega_mle): 1129.97

--------------------------------------------------------------------

Results for equation CO(GT)

==============================================================================

coefficient std. error t-stat prob

------------------------------------------------------------------------------

const 0.241332 0.069966 3.449 0.001

L1.CO(GT) 0.961418 0.019229 49.999 0.000

L1.NO2(GT) 0.001992 0.000713 2.794 0.005

L1.RH 0.009321 0.002735 3.409 0.001

L2.CO(GT) -0.279491 0.026156 -10.686 0.000

L2.NO2(GT) 0.000661 0.000970 0.682 0.495

L2.RH -0.017300 0.004278 -4.044 0.000

L3.CO(GT) 0.098032 0.026251 3.734 0.000

L3.NO2(GT) -0.000165 0.000970 -0.170 0.865

L3.RH 0.012764 0.004352 2.933 0.003

L4.CO(GT) -0.001012 0.026285 -0.038 0.969

L4.NO2(GT) -0.001148 0.000966 -1.189 0.234

L4.RH -0.006423 0.004354 -1.475 0.140

L5.CO(GT) 0.054358 0.026291 2.068 0.039

L5.NO2(GT) -0.001218 0.000966 -1.261 0.207

L5.RH 0.000664 0.004353 0.153 0.879

L6.CO(GT) -0.017663 0.026308 -0.671 0.502

L6.NO2(GT) 0.000372 0.000966 0.385 0.700

L6.RH 0.000884 0.004351 0.203 0.839

L7.CO(GT) 0.004448 0.026302 0.169 0.866

L7.NO2(GT) 0.000921 0.000967 0.953 0.340

L7.RH -0.000964 0.004353 -0.221 0.825

L8.CO(GT) -0.001457 0.026288 -0.055 0.956

L8.NO2(GT) 0.000736 0.000968 0.760 0.447

L8.RH -0.002357 0.004356 -0.541 0.588

L9.CO(GT) 0.018534 0.026296 0.705 0.481

L9.NO2(GT) -0.001551 0.000969 -1.601 0.109

L9.RH 0.004720 0.004361 1.082 0.279

L10.CO(GT) -0.003435 0.026289 -0.131 0.896

L10.NO2(GT) 0.001457 0.000969 1.503 0.133

L10.RH 0.003194 0.004366 0.732 0.464

L11.CO(GT) -0.021526 0.026286 -0.819 0.413

L11.NO2(GT) -0.001094 0.000969 -1.128 0.259

L11.RH -0.001129 0.004367 -0.259 0.796

L12.CO(GT) 0.066587 0.026287 2.533 0.011

L12.NO2(GT) -0.000285 0.000971 -0.293 0.769

L12.RH -0.002315 0.004369 -0.530 0.596

L13.CO(GT) -0.076568 0.026287 -2.913 0.004

L13.NO2(GT) 0.000551 0.000971 0.567 0.571

L13.RH 0.004622 0.004370 1.058 0.290

L14.CO(GT) 0.100874 0.026293 3.837 0.000

L14.NO2(GT) -0.003074 0.000971 -3.165 0.002

L14.RH 0.001720 0.004371 0.394 0.694

L15.CO(GT) -0.039783 0.026318 -1.512 0.131

L15.NO2(GT) 0.000926 0.000971 0.953 0.340

L15.RH -0.002928 0.004370 -0.670 0.503

L16.CO(GT) 0.009289 0.026276 0.354 0.724

L16.NO2(GT) 0.000818 0.000969 0.845 0.398

L16.RH -0.001466 0.004369 -0.336 0.737

L17.CO(GT) -0.030972 0.026264 -1.179 0.238

L17.NO2(GT) 0.000273 0.000969 0.281 0.778

L17.RH 0.000574 0.004369 0.131 0.895

L18.CO(GT) 0.021964 0.026242 0.837 0.403

L18.NO2(GT) -0.001183 0.000968 -1.222 0.222

L18.RH 0.003188 0.004366 0.730 0.465

L19.CO(GT) 0.048666 0.026200 1.858 0.063

L19.NO2(GT) -0.000539 0.000966 -0.558 0.577

L19.RH -0.010088 0.004362 -2.313 0.021

L20.CO(GT) -0.065842 0.026213 -2.512 0.012

L20.NO2(GT) 0.000847 0.000965 0.878 0.380

L20.RH 0.008736 0.004363 2.002 0.045

L21.CO(GT) -0.032047 0.026233 -1.222 0.222

L21.NO2(GT) 0.001082 0.000964 1.122 0.262

L21.RH -0.004805 0.004360 -1.102 0.270

L22.CO(GT) 0.050969 0.026220 1.944 0.052

L22.NO2(GT) -0.000471 0.000964 -0.489 0.625

L22.RH 0.000472 0.004360 0.108 0.914

L23.CO(GT) 0.071433 0.026226 2.724 0.006

L23.NO2(GT) 0.001170 0.000964 1.214 0.225

L23.RH -0.003465 0.004361 -0.794 0.427

L24.CO(GT) 0.198774 0.026160 7.598 0.000

L24.NO2(GT) -0.000280 0.000968 -0.289 0.772

L24.RH 0.001856 0.004361 0.425 0.670

L25.CO(GT) -0.156857 0.026043 -6.023 0.000

L25.NO2(GT) 0.000666 0.000967 0.689 0.491

L25.RH 0.000979 0.004290 0.228 0.820

L26.CO(GT) -0.047697 0.019186 -2.486 0.013

L26.NO2(GT) -0.001958 0.000710 -2.757 0.006

L26.RH -0.000747 0.002746 -0.272 0.786

==============================================================================

Results for equation NO2(GT)

==============================================================================

coefficient std. error t-stat prob

------------------------------------------------------------------------------

const 12.417213 1.871552 6.635 0.000

L1.CO(GT) 1.600229 0.514359 3.111 0.002

L1.NO2(GT) 0.953169 0.019069 49.986 0.000

L1.RH 0.239537 0.073150 3.275 0.001

L2.CO(GT) -2.404892 0.699653 -3.437 0.001

L2.NO2(GT) -0.096250 0.025935 -3.711 0.000

L2.RH -0.332820 0.114442 -2.908 0.004

L3.CO(GT) 0.154091 0.702192 0.219 0.826

L3.NO2(GT) 0.018241 0.025946 0.703 0.482

L3.RH 0.180558 0.116422 1.551 0.121

L4.CO(GT) 1.160555 0.703122 1.651 0.099

L4.NO2(GT) -0.065148 0.025831 -2.522 0.012

L4.RH -0.149770 0.116468 -1.286 0.198

L5.CO(GT) -0.209355 0.703264 -0.298 0.766

L5.NO2(GT) 0.007011 0.025834 0.271 0.786

L5.RH 0.023622 0.116443 0.203 0.839

L6.CO(GT) 0.742858 0.703728 1.056 0.291

L6.NO2(GT) -0.029688 0.025847 -1.149 0.251

L6.RH 0.014889 0.116384 0.128 0.898

L7.CO(GT) -0.535398 0.703562 -0.761 0.447

L7.NO2(GT) 0.089765 0.025857 3.472 0.001

L7.RH -0.106262 0.116432 -0.913 0.361

L8.CO(GT) -1.025553 0.703193 -1.458 0.145

L8.NO2(GT) -0.034196 0.025895 -1.321 0.187

L8.RH 0.127190 0.116517 1.092 0.275

L9.CO(GT) 0.313129 0.703395 0.445 0.656

L9.NO2(GT) 0.005236 0.025910 0.202 0.840

L9.RH -0.136264 0.116667 -1.168 0.243

L10.CO(GT) -0.507195 0.703213 -0.721 0.471

L10.NO2(GT) 0.000967 0.025922 0.037 0.970

L10.RH 0.209375 0.116786 1.793 0.073

L11.CO(GT) -1.319501 0.703135 -1.877 0.061

L11.NO2(GT) 0.069145 0.025930 2.667 0.008

L11.RH -0.053156 0.116828 -0.455 0.649

L12.CO(GT) 2.602906 0.703181 3.702 0.000

L12.NO2(GT) -0.076889 0.025968 -2.961 0.003

L12.RH -0.044469 0.116867 -0.381 0.704

L13.CO(GT) -2.098667 0.703156 -2.985 0.003

L13.NO2(GT) 0.068250 0.025986 2.626 0.009

L13.RH 0.164246 0.116893 1.405 0.160

L14.CO(GT) 1.141015 0.703317 1.622 0.105

L14.NO2(GT) -0.077485 0.025985 -2.982 0.003

L14.RH 0.121439 0.116918 1.039 0.299

L15.CO(GT) 0.157231 0.704010 0.223 0.823

L15.NO2(GT) 0.016822 0.025982 0.647 0.517

L15.RH -0.173595 0.116888 -1.485 0.138

L16.CO(GT) 0.878201 0.702861 1.249 0.211

L16.NO2(GT) 0.003234 0.025923 0.125 0.901

L16.RH -0.029109 0.116858 -0.249 0.803

L17.CO(GT) -1.418159 0.702559 -2.019 0.044

L17.NO2(GT) 0.016251 0.025913 0.627 0.531

L17.RH -0.015862 0.116863 -0.136 0.892

L18.CO(GT) 0.655452 0.701962 0.934 0.350

L18.NO2(GT) -0.021180 0.025901 -0.818 0.414

L18.RH 0.128568 0.116801 1.101 0.271

L19.CO(GT) -0.024839 0.700835 -0.035 0.972

L19.NO2(GT) 0.001731 0.025844 0.067 0.947

L19.RH -0.247871 0.116687 -2.124 0.034

L20.CO(GT) -0.810637 0.701198 -1.156 0.248

L20.NO2(GT) 0.008661 0.025806 0.336 0.737

L20.RH 0.082541 0.116699 0.707 0.479

L21.CO(GT) -0.268031 0.701722 -0.382 0.702

L21.NO2(GT) 0.006716 0.025794 0.260 0.795

L21.RH -0.148403 0.116634 -1.272 0.203

L22.CO(GT) 0.551561 0.701384 0.786 0.432

L22.NO2(GT) 0.029776 0.025786 1.155 0.248

L22.RH 0.137999 0.116639 1.183 0.237

L23.CO(GT) 0.396023 0.701541 0.565 0.572

L23.NO2(GT) 0.141030 0.025786 5.469 0.000

L23.RH -0.095500 0.116666 -0.819 0.413

L24.CO(GT) 0.359015 0.699771 0.513 0.608

L24.NO2(GT) 0.081228 0.025886 3.138 0.002

L24.RH 0.027786 0.116658 0.238 0.812

L25.CO(GT) -1.491610 0.696641 -2.141 0.032

L25.NO2(GT) -0.067370 0.025857 -2.605 0.009

L25.RH -0.015628 0.114756 -0.136 0.892

L26.CO(GT) 0.583311 0.513221 1.137 0.256

L26.NO2(GT) -0.100912 0.018999 -5.311 0.000

L26.RH 0.021928 0.073465 0.298 0.765

==============================================================================

Results for equation RH

==============================================================================

coefficient std. error t-stat prob

------------------------------------------------------------------------------

const 1.708989 0.393111 4.347 0.000

L1.CO(GT) -0.043025 0.108039 -0.398 0.690

L1.NO2(GT) -0.010353 0.004005 -2.585 0.010

L1.RH 1.209022 0.015365 78.688 0.000

L2.CO(GT) -0.237686 0.146959 -1.617 0.106

L2.NO2(GT) 0.010539 0.005448 1.935 0.053

L2.RH -0.290694 0.024038 -12.093 0.000

L3.CO(GT) 0.154914 0.147492 1.050 0.294

L3.NO2(GT) -0.002859 0.005450 -0.525 0.600

L3.RH 0.052192 0.024454 2.134 0.033

L4.CO(GT) 0.095980 0.147688 0.650 0.516

L4.NO2(GT) 0.003434 0.005426 0.633 0.527

L4.RH -0.021893 0.024464 -0.895 0.371

L5.CO(GT) -0.035423 0.147718 -0.240 0.810

L5.NO2(GT) -0.002389 0.005426 -0.440 0.660

L5.RH 0.037941 0.024458 1.551 0.121

L6.CO(GT) -0.040464 0.147815 -0.274 0.784

L6.NO2(GT) 0.001410 0.005429 0.260 0.795

L6.RH -0.074252 0.024446 -3.037 0.002

L7.CO(GT) -0.012767 0.147780 -0.086 0.931

L7.NO2(GT) 0.007474 0.005431 1.376 0.169

L7.RH 0.040664 0.024456 1.663 0.096

L8.CO(GT) 0.080673 0.147703 0.546 0.585

L8.NO2(GT) 0.001860 0.005439 0.342 0.732

L8.RH -0.076619 0.024474 -3.131 0.002

L9.CO(GT) 0.047686 0.147745 0.323 0.747

L9.NO2(GT) -0.004802 0.005442 -0.882 0.378

L9.RH 0.063403 0.024505 2.587 0.010

L10.CO(GT) 0.050348 0.147707 0.341 0.733

L10.NO2(GT) 0.004929 0.005445 0.905 0.365

L10.RH -0.044706 0.024530 -1.822 0.068

L11.CO(GT) 0.117202 0.147691 0.794 0.427

L11.NO2(GT) -0.002450 0.005446 -0.450 0.653

L11.RH 0.050771 0.024539 2.069 0.039

L12.CO(GT) 0.081156 0.147700 0.549 0.583

L12.NO2(GT) -0.002690 0.005454 -0.493 0.622

L12.RH -0.040349 0.024547 -1.644 0.100

L13.CO(GT) -0.028788 0.147695 -0.195 0.845

L13.NO2(GT) 0.000768 0.005458 0.141 0.888

L13.RH 0.020414 0.024553 0.831 0.406

L14.CO(GT) -0.078942 0.147729 -0.534 0.593

L14.NO2(GT) -0.002734 0.005458 -0.501 0.616

L14.RH -0.000282 0.024558 -0.011 0.991

L15.CO(GT) -0.144161 0.147874 -0.975 0.330

L15.NO2(GT) 0.002442 0.005457 0.448 0.654

L15.RH 0.030373 0.024552 1.237 0.216

L16.CO(GT) -0.001777 0.147633 -0.012 0.990

L16.NO2(GT) 0.002061 0.005445 0.379 0.705

L16.RH -0.049313 0.024546 -2.009 0.045

L17.CO(GT) 0.046799 0.147569 0.317 0.751

L17.NO2(GT) -0.007569 0.005443 -1.391 0.164

L17.RH 0.033906 0.024547 1.381 0.167

L18.CO(GT) -0.080688 0.147444 -0.547 0.584

L18.NO2(GT) 0.006073 0.005440 1.116 0.264

L18.RH 0.006116 0.024533 0.249 0.803

L19.CO(GT) 0.269110 0.147207 1.828 0.068

L19.NO2(GT) -0.004253 0.005429 -0.784 0.433

L19.RH -0.011621 0.024510 -0.474 0.635

L20.CO(GT) -0.324511 0.147284 -2.203 0.028

L20.NO2(GT) 0.000789 0.005420 0.145 0.884

L20.RH 0.041952 0.024512 1.711 0.087

L21.CO(GT) 0.177418 0.147394 1.204 0.229

L21.NO2(GT) 0.005398 0.005418 0.996 0.319

L21.RH -0.037378 0.024499 -1.526 0.127

L22.CO(GT) 0.124107 0.147323 0.842 0.400

L22.NO2(GT) -0.006135 0.005416 -1.133 0.257

L22.RH 0.041857 0.024500 1.708 0.088

L23.CO(GT) -0.041076 0.147356 -0.279 0.780

L23.NO2(GT) -0.005205 0.005416 -0.961 0.337

L23.RH 0.047960 0.024505 1.957 0.050

L24.CO(GT) 0.171936 0.146984 1.170 0.242

L24.NO2(GT) 0.003821 0.005437 0.703 0.482

L24.RH 0.010637 0.024503 0.434 0.664

L25.CO(GT) -0.302108 0.146326 -2.065 0.039

L25.NO2(GT) 0.007458 0.005431 1.373 0.170

L25.RH -0.034121 0.024104 -1.416 0.157

L26.CO(GT) 0.150202 0.107800 1.393 0.164

L26.NO2(GT) -0.008683 0.003991 -2.176 0.030

L26.RH -0.041247 0.015431 -2.673 0.008

==============================================================================

Correlation matrix of residuals

CO(GT) NO2(GT) RH

CO(GT) 1.000000 0.606004 0.150771

NO2(GT) 0.606004 1.000000 0.078143

RH 0.150771 0.078143 1.000000

4. Get forecast¶

forecast_var = pd.DataFrame(var_model.forecast(train_df.values,

steps=forecast_length),

columns=train_df.columns,

index=test_df.index)

forecast_var = forecast_var.rename(columns={c: c+'-VAR' for c in forecast_var.columns})

for c in train_df.columns:

fig, ax = plt.subplots(figsize=[15, 2])

pd.concat([train_df[[c]], forecast_var[[c+'-VAR']]], axis=1).plot(ax=ax)

plt.xlim(left=pd.to_datetime('2005-03-01'))

plt.xlabel('')

# plt.tight_layout()

plt.show()

Performance Evaluation: Comparison with ARIMA model¶

When using ARIMA, we treat each variable as a univariate time series, and we perform the forecasting for each variable: 1 for CO, 1 for NO2, and 1 for RH

# For model order selection, refer to Chapter 1

selected_order = {'CO(GT)': [(0, 1, 0)],

'NO2(GT)': [(0, 1, 0)],

'RH': [(3, 1, 1)]}

%%time

forecast_arima = {}

for c in cols:

forecast_arima[c+'-ARIMA'] = utils.forecast_arima(train_df[c].values,

test_df[c].values,

order=selected_order[c][0])

forecast_arima = pd.DataFrame(forecast_arima, index=forecast_var.index)

forecast_arima.head()

CPU times: user 4.32 s, sys: 268 ms, total: 4.58 s

Wall time: 1.48 s

| CO(GT)-ARIMA | NO2(GT)-ARIMA | RH-ARIMA | |

|---|---|---|---|

| Date_Time | |||

| 2005-04-03 15:00:00 | 0.999865 | 87.002935 | 14.502893 |

| 2005-04-03 16:00:00 | 0.999729 | 87.005870 | 16.743239 |

| 2005-04-03 17:00:00 | 0.999594 | 87.008806 | 19.253414 |

| 2005-04-03 18:00:00 | 0.999458 | 87.011741 | 21.715709 |

| 2005-04-03 19:00:00 | 0.999323 | 87.014676 | 23.974483 |

forecasts = pd.concat([forecast_arima, forecast_var], axis=1)

for c in cols:

fig, ax = utils.plot_forecasts_static(train_df=train_df,

test_df=test_df,

forecast_df=forecasts,

column_name=c,

min_train_date='2005-04-01',

suffix=['-VAR', '-ARIMA'],

title=c)

Performance Metrics

pd.concat([utils.test_performance_metrics(test_df, forecast_var, suffix='-VAR'),

utils.test_performance_metrics(test_df, forecast_arima, suffix='-ARIMA')], axis=1)

| CO(GT)-VAR | NO2(GT)-VAR | RH-VAR | CO(GT)-ARIMA | NO2(GT)-ARIMA | RH-ARIMA | |

|---|---|---|---|---|---|---|

| MAE | 0.685005 | 31.687612 | 9.748883 | 1.057097 | 59.283376 | 16.239017 |

| MSE | 1.180781 | 1227.046604 | 111.996306 | 2.163021 | 4404.904459 | 333.622140 |

| MAPE | 43.508500 | 29.811066 | 35.565987 | 56.960617 | 46.190671 | 51.199023 |

Observation/s:

MAE: VAR forecasts have lower errors than ARIMA forecasts for CO and NO2 but not in RH.

MSE: VAR forecasts have lower errors for all variables (CO, NO2 and RH).

MAPE: VAR forecasts have lower errors for all variables (CO, NO2 and RH).

Training time is significantly reduced when using VAR compared to ARIMA (<0.1s run time for VAR while ~20s for ARIMA)

Structural VAR Analysis¶

In addition to forecasting, VAR models are also used for structural inference and policy analysis. In macroeconomics, this structural analysis has been extensively employed to investigate the transmission mechanisms of macroeconomic shocks (e.g., monetary shocks, financial shocks) and test economic theories. There are particular assumptions imposed about the causal structure of the dataset, and the resulting causal impacts of unexpected shocks (also called innovations or perturbations) to a specific variable on the different variables in the model are summarized. In this section, we cover two of the common methods in summarizing the effects of these causal impacts: (1) impulse response functions, and (2): forecast error variance decompositions.

Impulse Response Function (IRF)¶

Coefficients of the VAR models are often difficult to interpret so practitioners often estimate the impulse response function.

IRFs trace out the time path of the effects of an exogenous shock to one (or more) of the endogenous variables on some or all of the other variables in a VAR system.

IRF traces out the response of the dependent variable of the VAR system to shocks (also called innovations or impulses) in the error terms.

IRF in the VAR system for Air Quality¶

Let \(y_{1,t}\), \(y_{2,t}\) and \(y_{3,t}\) be the time series corresponding to CO signal, NO2 signal, and RH signal, respectively. Consider the moving average representation of the system shown below:

Let

Suppose \(u_1\) in the first equation increases by a value of one standard deviation.

This shock will change \(y_1\) in the current as well as the future periods.

This shock will also have an impact on \(y_2\) and \(y_3\).

Suppose \(u_2\) in the second equation increases by a value of one standard deviation.

This shock will change \(y_2\) in the current as well as the future periods.

This shock will also have an impact on \(y_1\) and \(y_3\).

Suppose \(u_3\) in the third equation increases by a value of one standard deviation.

This shock will change \(y_3\) in the current as well as the future periods.

This shock will also have an impact on \(y_1\) and \(y_2\).

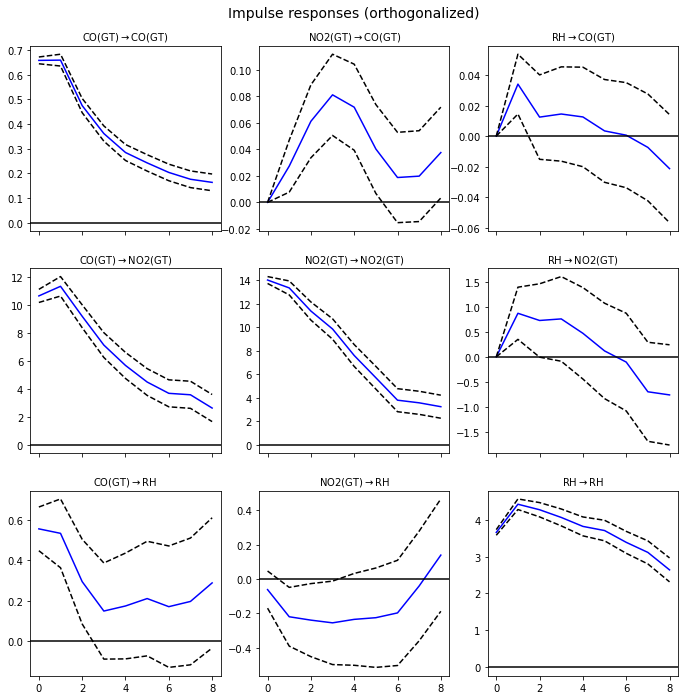

irf = var_model.irf(periods=8)

ax = irf.plot(orth=True,

subplot_params={'fontsize': 10})

Observation/s:

Effects of exogenous perturbation/shocks (1SD) of a variable on itself:

CO \(\rightarrow\) CO: A shock in the value of CO has a larger effect CO in the early hours but this decays over time.

NO2 \(\rightarrow\) NO2: A shock in the value of NO2 has a larger effect NO2 in the early hours but this decays over time.

RH \(\rightarrow\) RH: A shock in the value of RH has a largest effect in RH after 1 hour and this effect decays over time.

Effects of exogenous perturbation/shocks of a variable on another:

CO \(\rightarrow\) NO2: A shock in the value of CO has a largest effect in NO2 after 1 hour and this effect decays over time.

CO \(\rightarrow\) RH: A shock in the value of CO has an immediate effect in the value of RH. However, the effect decreases immediately after an hour, and the value seems to stay at around 0.2.

NO2 \(\rightarrow\) CO: A shock in NO2 only causes a small effect in the values of CO. There seems to be a delayed effect, peaking after 3 hours, but the magnitude is still small.

NO2 \(\rightarrow\) RH: A shock in NO2 causes a small (negative) effect in the values of RH. The magnitude seems to decline further after 6 hours. The value of the IRF reaches zero in about 7 hours.

RH \(\rightarrow\) CO: A shock in RH only causes a small effect in the values of CO.

RH \(\rightarrow\) NO2: A shock in the value of RH has a largest effect in NO2 after 1 hour and this effect decays over time. The value of the IRF reaches zero after 6 hours.

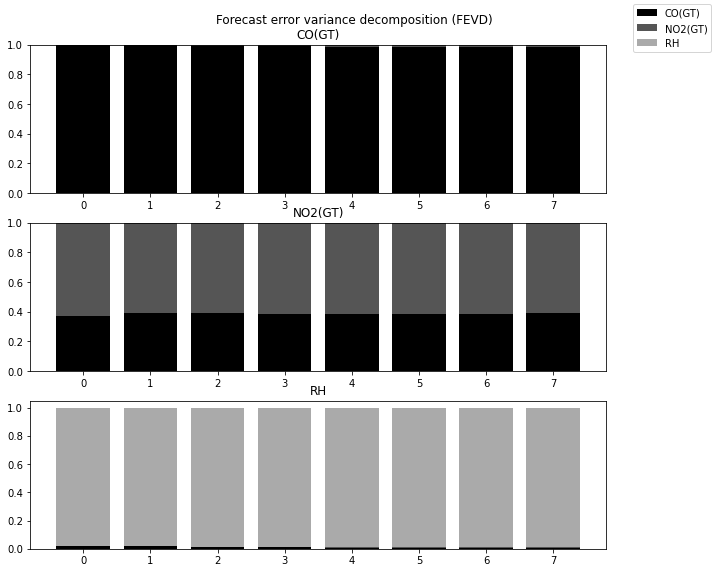

Forecast Error Variance Decomposition (FEVD)¶

FEVD indicates the amount of information each variable contributes to the other variables in the autoregression

While impulse response functions trace the effects of a shock to one endogenous variable on to the other variables in the VAR, variance decomposition separates the variation in an endogenous variable into the component shocks to the VAR.

It determines how much of the forecast error variance of each of the variables can be explained by exogenous shocks to the other variables.

fevd = var_model.fevd(8)

ax = fevd.plot(figsize=(10, 8))

plt.show()

Observation/s:

For CO, the variance is mostly explained by exogenous shocks to CO. This decreases over time but only by a small amount.

For NO2, the variance is mostly explained by exogenous shocks to NO2 and CO.

For RH, the variance is mostly explained by exogenous shocks to RH. Over time, the contribution of the exogenous shocks to CO increases.

Example 3: Forecasting the Jena climate data¶

We try to forecast the Jena climate data using the method outlined above. We will train the VAR model using hourly weather measurements from January 1, 2019 (00:10) up to December 29, 2014 (18:10). The performance of the model will be evaluated on the test set which contains data from December 29, 2014 (19:10) to December 31, 2014 (23:20) which is equivalent to 17,523 data points for each of the variables.

Load dataset¶

train_df = pd.read_csv('../data/train_series_datetime.csv',index_col=0).set_index('Date Time')

val_df = pd.read_csv('../data/val_series_datetime.csv',index_col=0).set_index('Date Time')

test_df = pd.read_csv('../data/test_series_datetime.csv',index_col=0).set_index('Date Time')

train_df.index = pd.to_datetime(train_df.index)

val_df.index = pd.to_datetime(val_df.index)

test_df.index = pd.to_datetime(test_df.index)

train_val_df = pd.concat([train_df, val_df])

Check stationarity of each variable using ADF test¶

%%time

test_stat, p_val = [], []

cv_1pct, cv_5pct, cv_10pct = [], [], []

for c in train_val_df.columns:

adf_res = adfuller(train_val_df[c].dropna())

test_stat.append(adf_res[0])

p_val.append(adf_res[1])

cv_1pct.append(adf_res[4]['1%'])

cv_5pct.append(adf_res[4]['5%'])

cv_10pct.append(adf_res[4]['10%'])

adf_res_df = pd.DataFrame({'Test statistic': test_stat,

'p-value': p_val,

'Critical value - 1%': cv_1pct,

'Critical value - 5%': cv_5pct,

'Critical value - 10%': cv_10pct},

index=train_df.columns).T

adf_res_df.round(4)

CPU times: user 3min 11s, sys: 25.8 s, total: 3min 37s

Wall time: 57.2 s

| p (mbar) | T (degC) | Tpot (K) | Tdew (degC) | rh (%) | VPmax (mbar) | VPact (mbar) | VPdef (mbar) | sh (g/kg) | H2OC (mmol/mol) | rho (g/m**3) | wv (m/s) | max. wv (m/s) | wd (deg) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Test statistic | -15.5867 | -7.9586 | -8.3354 | -8.5750 | -17.7069 | -9.1945 | -9.0103 | -13.5492 | -9.0827 | -9.0709 | -9.3980 | -24.2424 | -24.3052 | -19.8394 |

| p-value | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Critical value - 1% | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 | -3.4305 |

| Critical value - 5% | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 | -2.8616 |

| Critical value - 10% | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 | -2.5668 |

((adf_res_df.loc['Test statistic']< adf_res_df.loc['Critical value - 1%']) &

(adf_res_df.loc['Test statistic']< adf_res_df.loc['Critical value - 5%']) &

( adf_res_df.loc['Test statistic']< adf_res_df.loc['Critical value - 10%']))

p (mbar) True

T (degC) True

Tpot (K) True

Tdew (degC) True

rh (%) True

VPmax (mbar) True

VPact (mbar) True

VPdef (mbar) True

sh (g/kg) True

H2OC (mmol/mol) True

rho (g/m**3) True

wv (m/s) True

max. wv (m/s) True

wd (deg) True

dtype: bool

Observation/s:

From the values above, all the components of the Jena climate data are stationary, so we’ll use all the variables in our VAR model.

Select order p¶

%%time

aic, bic, fpe, hqic = [], [], [], []

model = VAR(train_val_df)

p = np.arange(1,60)

for i in p:

result = model.fit(i)

aic.append(result.aic)

bic.append(result.bic)

fpe.append(result.fpe)

hqic.append(result.hqic)

lags_metrics_df = pd.DataFrame({'AIC': aic,

'BIC': bic,

'HQIC': hqic,

'FPE': fpe},

index=p)

fig, ax = plt.subplots(1, 4, figsize=(15, 3), sharex=True)

lags_metrics_df.plot(subplots=True, ax=ax, marker='o')

plt.tight_layout()

CPU times: user 2min 57s, sys: 14.3 s, total: 3min 11s

Wall time: 1min

lags_metrics_df.idxmin()

AIC 51

BIC 5

HQIC 26

FPE 51

dtype: int64

lags_metrics_df[25:].idxmin()

AIC 51

BIC 26

HQIC 26

FPE 51

dtype: int64

Observation/s:

The model order that resulted to the minimum value varies for each information criteria, showing no clear minimum. We see an elbow at \(p=5\), but if we look at AIC and HQIC we’re observing another elbow/local minimum at \(p=26\). So, we choose \(p=26\) as our lag length.

Train VAR model using the training and validation data¶

%%time

var_model = model.fit(26)

CPU times: user 1.38 s, sys: 151 ms, total: 1.53 s

Wall time: 631 ms

test_index = np.arange(len(test_df)- (len(test_df))%24).reshape((-1, 24))

fit_index = [test_index[:i].flatten() for i in range(len(test_index))]

Forecast 24-hour weather measurements and evaluate performance on test set¶

forecasts_df = []

for n in range(len(fit_index)):

forecast_var = pd.DataFrame(var_model.forecast(

pd.concat([train_val_df, test_df.iloc[fit_index[n]]]).values, steps=24),

columns=train_val_df.columns,

index=test_df.iloc[test_index[n]].index)

forecasts_df.append(forecast_var)

forecasts_df = pd.concat(forecasts_df)

forecasts_df.columns = forecasts_df.columns+['-VAR']

for c in train_val_df.columns:

fig, ax = plt.subplots(figsize=[14, 2])

train_val_df[c].plot(ax=ax)

forecasts_df[[c+'-VAR']].plot(ax=ax)

plt.ylim(train_val_df[c].min(), train_val_df[c].max())

plt.legend(loc=2)

plt.tight_layout()

plt.show()

Evaluate forecasts

utils.test_performance_metrics(test_df.loc[forecasts_df.index], forecasts_df, suffix='-VAR').loc[['MAE', 'MSE']]

| p (mbar)-VAR | T (degC)-VAR | Tpot (K)-VAR | Tdew (degC)-VAR | rh (%)-VAR | VPmax (mbar)-VAR | VPact (mbar)-VAR | VPdef (mbar)-VAR | sh (g/kg)-VAR | H2OC (mmol/mol)-VAR | rho (g/m**3)-VAR | wv (m/s)-VAR | max. wv (m/s)-VAR | wd (deg)-VAR | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MAE | 2.681284 | 2.542025 | 2.603187 | 1.797102 | 10.899944 | 2.526237 | 1.171625 | 2.379343 | 0.744665 | 1.186948 | 12.164486 | 3.136091 | 4.414089 | 66.420597 |

| MSE | 238.321753 | 652.733627 | 618.458262 | 102.257346 | 9581.665059 | 540.666240 | 39.837241 | 490.874048 | 15.612470 | 39.678736 | 9986.126326 | 17352.964659 | 23404.318476 | 87581.698748 |

T_MAEs = []

for n in range(len(test_index)):

index = forecasts_df.iloc[test_index[n]].index

T_MAEs.append(utils.mean_absolute_error(test_df.loc[index, 'T (degC)'].values,

forecasts_df.loc[index, 'T (degC)-VAR'].values))

print(f'VAR(26) MAE: {np.mean(T_MAEs)}')

VAR(26) MAE: 2.5420250169753875

Observation/s: The VAR(26) model outperformed the naive (MAE= 3.18), seasonal naive (MAE= 2.61) and ARIMA (MAE= 3.19) models.

Forecast 24 hours beyond test set¶

all_data = pd.concat([train_df, val_df, test_df])

future_index = [all_data.index[-1]+pd.Timedelta(f'{h} hour') for h in np.arange(24)+1]

forecast_var_future = pd.DataFrame(var_model.forecast(all_data.values,

steps=24),

columns=all_data.columns,

index=future_index)

forecast_var_future.columns = forecast_var_future.columns+['-VAR']

for c in train_val_df.columns:

fig, ax = plt.subplots(figsize=[14, 2])

all_data.iloc[-500:][c].plot(ax=ax)

forecast_var_future[[c+'-VAR']].plot(ax=ax)

plt.ylim(train_val_df[c].min(), train_val_df[c].max())

plt.legend(loc=2)

plt.tight_layout()

plt.show()

Summary¶

VAR methods are useful when dealing with multivariate time series, as they allow us to use the relationship between the different variable to forecast.

These models allow us to forecast the different variables simultaneously, with the added benefit of easy (only 1 hyperparameter) and fast training.

Using the fitted VAR model, we can also explain the relationship between variables, and how the perturbation in one variable affects the others by getting the impulse response functions and the variance decomposition of the forecasts.

However, the application of these models is limited due to the stationarity requirement for ALL the variables in the multivariate time series. This method won’t work well if there is at least one variable that’s non-stationary. When dealing with non-stationary multivariate time series, one can explore the use of vector error correction models (VECM).

Preview to the Next Chapter¶

In the next chapter, we further extend the use of VAR models to explain the relationships between variables in a multivariate time series using Granger causality, which is one of the most common ways to describe causal mechanisms in time series data.

References¶

Main references

Lütkepohl, H. (2005). New introduction to multiple time series analysis. Berlin: Springer.

Kilian, L., & Lütkepohl, H. (2018). Structural vector autoregressive analysis. Cambridge: Cambridge University Press.

Supplementary references are listed here.